Audit of the Procurement Phase of the New Bridge for the St. Lawrence Corridor Project - Contract Management

April 2015

Table of Contents

- Executive Summary

- Background

- Audit Objective and Scope

- Audit Approach

- Audit Findings

- Conclusion and Recommendations

- Statement of Conformance

- Management Response and Action Plan

1 EXECUTIVE SUMMARY

Introduction

On October 5, 2011, the Government of Canada announced that the Champlain Bridge over the St. Lawrence River between the cities of Montreal and Brossard would be replaced by a new crossing. The New Bridge for the St. Lawrence Corridor (NBSLC) Project is one of the largest current infrastructure projects in North America. The NBSLC project includes building a new bridge, reconstructing and widening the federal portion of Highway A15 and replacing the Nun's Island Bridge.

On February 13, 2014, project authority was transferred from the Minister of Transport to the Minister of Infrastructure, Communities, and Intergovernmental Affairs, and Minister of the Economic Development Agency of Canada for the Regions of Quebec. This established Infrastructure Canada as the lead organization responsible for overseeing and managing the NBSLC project. The Department has worked in an integrated manner with officials from the contracting authority, Public Works and Government Services Canada as well as with Public Private Partnerships Canada, and with legal advisors from the Department of Justice.

Audit Objective and Scope

The audit objective was to assess contract management controls of contracts supporting the Procurement Phase of the New Bridge for the St. Lawrence Corridor Project.

The audit criteria are:

- Contract management and monitoring practices complied with Government of Canada legislation as well as Treasury Board and Infrastructure Canada policies and directives; and

- Processes in place to pay for goods and services delivered complied with Government of Canada legislation as well as Treasury Board and Infrastructure Canada policies and directives.

The audit scope focused on Infrastructure Canada's role since it assumed responsibility for the NBSLC project in February 2014, including becoming the technical authority for contracting purposes. Specifically, the audit examined the controls and processes established for contract amendments and payments for goods and services received between May 2014 and November 2014, when Infrastructure Canada assumed full administrative responsibility for the project.

Conclusion

Overall, contract management and monitoring practices were generally compliant with relevant authorities and policies. However, the implementation of the controls established to pay for goods and services received were not fully compliant with legislative and policy requirements. Immediate measures should be put in place to ensure that departmental financial delegations are working as intended. This includes strengthening controls related to section 33 and 34 of the Financial Administration Act.

There are two recommendations:

- The Assistant Deputy Minister, Corporate Services Branch should ensure that Federal Montreal Bridges Branch officials responsible for contracts are trained on appropriate standard contract management practices and processes, including FAA signatory requirements and the management of contract amendments.

- The Assistant Deputy Minister, Corporate Services Branch should establish controls to strengthen the section 33 approval process and to ensure that payments are authorized by an official with the appropriate delegated authority as per the departmental delegation of financial signing authorities.

Management response: Management accepts the recommendations and action plans have been put in place to address the two areas for improvement identified.

The audit findings, conclusions and recommendations relate only to Infrastructure Canada and do not reflect the management practices employed by any other department.

2 BACKGROUND

The current Champlain Bridge over the St. Lawrence River which links the cities of Montreal and Brossard, was put into service in June 1962. In 2011, the Jacques Cartier and Champlain Bridges Incorporated, which owns and operates the existing Champlain Bridge, commissioned an engineering study jointly with the Ministère des Transports du Québec, which concluded that the bridge should be replaced as soon as possible. As a result, the Government of Canada approved a bridge replacement project later that year.

Canada's Economic Action Plan 2013 confirmed investments for various infrastructure projects, including the replacement of the Champlain Bridge. The New Bridge for the St. Lawrence Corridor project includes building a new bridge, reconstructing and widening the federal portion of Highway A15, and replacing the Nun's Island Bridge. Responsibility for the NBSLC project was assigned to Transport Canada.

Later that year, a new accelerated timeline of 2018 was established for the completion of the bridge portion of the NBSLC project, three years earlier than previously planned. At the initial stages of the NBSLC project, Transport Canada worked closely with Public Works and Government Services Canada (PWGSC) to obtain the necessary project approvals. A Government of Canada strategic decision was made to procure the NBSLC project as a public-private partnership.

On February 13, 2014, the NBSLC project authority was transferred from the Minister of Transport to the Minister of Infrastructure, Communities, and Intergovernmental Affairs, and Minister of the Economic Development Agency of Canada for the Regions of Quebec. This established Infrastructure Canada as the lead organization and project authority responsible for overseeing and managing the NBSLC project. Infrastructure Canada worked in an integrated manner with officials from the contracting authority PWGSC, as well as with Public Private Partnerships Canada, and with legal advisors from the Department of Justice.

A Memorandum of Understanding between Infrastructure Canada and Transport Canada was developed to facilitate the provision of internal services during the transition period which ended in May 2014.

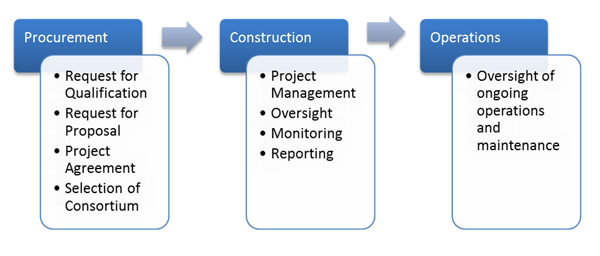

The NBSLC project had three distinct phases (Figure 1).

Figure 1: Three project phases

The period audited covered contracts entered into during the procurement phase of the project. As of November 30, 2014, Infrastructure Canada was responsible for managing nine contracts related to the procurement phase of the project with a current value of approximately $23 million. Of those, eight contracts were developed under the technical authority of Transport Canada and responsibility for these was transferred to Infrastructure Canada. These are included in the audit. The other contract, let by Infrastructure Canada, was of minimal value and had no activity during the audit period and was not included.

3 AUDIT OBJECTIVE AND SCOPE

The audit objective was to assess contract management controls of contracts supporting the Procurement Phase of the New Bridge for the St. Lawrence Corridor Project.

The audit criteria are:

- Contract management and monitoring practices complied with Government of Canada legislation as well as Treasury Board and Infrastructure Canada policies and directives; and

- Processes in place to pay for goods and services delivered complied with Government of Canada legislation as well as Treasury Board and Infrastructure Canada policies and directives.

The audit scope focused on Infrastructure Canada's role since it assumed responsibility for the NBSLC project in February 2014, including becoming the technical authority for contracting purposes. Specifically, we assessed the controls and processes established for contract amendments and payments for goods and services received between May 2014 and November 2014, when Infrastructure Canada assumed full administrative responsibility for the project.

4 AUDIT APPROACH

The approach and methodology used conforms to generally accepted practices, processes, procedures and standards of internal audit in the Government of Canada, and conforms to the Treasury Board Policy on Internal Audit and the Institute of Internal Auditors International Standards for the Professional Practice of Internal Auditing. Audit criteria were sourced from the Federal Administration Act, Treasury Board Contracting Policy, Directive on Delegation of Financial Authorities for Disbursements and Directive on Account Verification, as well as relevant elements of the Office of the Comptroller General's Audit Criteria Related to the Management Accountability Framework.

The audit work was conducted in three phases - planning, examination, and reporting - with deliverables prepared at key points. The planning phase included interviews with officials from Infrastructure Canada and Public Works and Government Services Canada, documentation reviews and an audit risk assessment. This knowledge formed the basis for determining the areas for detailed review in the examination phase.

The audit team worked closely with officials from the Office of Audit and Evaluation at Public Works and Government Services Canada to ensure a coordinated approach to fulfilling auditing requirements related to the project. It was determined that Infrastructure Canada's audit work would focus on the technical authority role while Public Works and Government Services' audit work would assess its role as contracting authority for the procurements in the preparatory phase of the New Bridge for the St. Lawrence Corridor (NBSLC) Project, as well as for a selection of contracts in support of the main bridge project.

In total, nine contracts were managed by Infrastructure Canada during the period under audit. In order to assess contract management and payment processes we selected judgmental samples from eight contracts, which represented approximately 99 percent of the overall total contract value. The samples included the following elements:

- Amendments. Eighteen amendments were processed for seven contracts managed by Infrastructure Canada between May and November 2014. One contract had no amendments. Seven amendments were classified as administrative (i.e. name and address changes). Eleven were non-administrative (i.e. changes to scope of work, deliverables, etc.). All 11 non-administrative amendments were included in the sample.

- Payments. In total there were 43 line items related to 32 unique invoices in the financial system related to seven of the eight contracts. One contract had no payments. We assessed 23 line items related to 23 unique invoices.

Preliminary audit findings were communicated to the auditee to validate facts and to confirm the clarity, accuracy, and completeness of the information reported.

5 AUDIT FINDINGS

5.1 Contract Management and Monitoring Practices

It was expected that:

- Contract management and monitoring practices complied with Government of Canada legislation as well as Treasury Board and Infrastructure Canada policies and directives.

Contract Management and Monitoring Practices

Conclusion:

Contract management and monitoring practices related to contracts supporting the procurement process of the project were generally compliant with relevant authorities and procedures. Two structural areas for improvement were identified related to file management and ensuring consistency amongst dollar amounts indicated on approved requisition forms, signed contracts and data entries in the departmental financial system.

Project and contract management authorities for 5.1 Contract Management and Monitoring Practices

Transport Canada was the responsible department at project initiation. In February 2014, Infrastructure Canada assumed overall responsibility for the NBSLC project.

The Treasury Board Contracting Policy outlines two specific roles related to contracting described below.

Contracting authority. The contracting authority has authority to bind Canada in a legal contract. For the contracts examined in this audit, PWGSC was contracting authority and procured the goods and services on behalf of Infrastructure Canada.

Technical authority. The technical authority develops the technical specifications and business requirements related to contracting for goods and services. Infrastructure Canada is the technical authority for the contracts examined in this audit. Federal Montreal Bridges Branch employees are responsible for developing the technical specifications and business requirements. Corporate Services Branch, Finance and Contracting Directorate officers are responsible for overall departmental contract management and for making payments for goods or services received once approved by officials with delegated authority.

The transition period for 5.1 Contract Management and Monitoring Practices

Between February and May 2014, corporate services officials from Transport Canada and Infrastructure Canada held discussions and meetings to support the transition of project authority. A Memorandum of Understanding was established to ensure that contract files were managed during the transition period and payments could be made by Transport Canada. The transition of files and personnel was completed in May 2014.

Confirming Order for 5.1 Contract Management and Monitoring Practices

The Federal Administration Act specifies that any payment related to a contract must be in accordance with the terms of that contact. When the contracting files were transferred to Infrastructure Canada, there were outstanding invoices for work previously performed. While most of the invoices were for work in accordance with the service contract, two invoices were for work that had been performed but assessed as not meeting contract specifications. Project team staff had requested the work from the supplier without first creating a required task authorization or official contract amendment. In order to address this situation, a confirming order was created so that payment could be made on the two invoices.

A confirming order is a payment mechanism that is used in exceptional circumstances to allow for payment of invoices related to work performed by a supplier without a contract. It should be noted that a confirming order is not a mechanism to initiate a contract. The departmental Procurement Review Committee supported the payment of the invoice through this method. The committee also requested that measures be put in place to prevent this from re-occurring. The project team established a new procedure and control point so that only one project team member coordinates all work related to this contract and this information has been communicated to the contractor.

Contract information management for 5.1 Contract Management and Monitoring Practices

Infrastructure Canada has a centralized contracting function that is managed by the Finance and Contracting Directorate. Standard business processes have been established to maintain all departmental procurement files within the Directorate so that officials who are responsible for managing contractual commitments in the departmental financial system have all the necessary information to fulfill their responsibilities.

Contract Amendments for 5.1 Contract Management and Monitoring Practices

Between May and November 30, 2014, there were 18 contract amendments related to the seven (7) contracts reviewed as part of this audit. Of the 18 amendments, seven (7) were administrative and 11 were non-administrative. Administrative amendment refers to items such as changing the name or address of signatories, updating the list of approved resources, or other similar changes. Non-administrative amendment refers to any changes related to the scope of work, deliverables and associated dollar values.

Contract amendment authorities and justifications for 5.1 Contract Management and Monitoring Practices

All 11 non-administrative contract amendments were performed accurately and documentation was on file to support and justify the decision to amend. In addition, there was evidence that PWGSC officials also approved the amendments in their capacity as contracting authority.

Contract amendment procedures for 5.1 Contract Management and Monitoring Practices

The Treasury Board Contracting Policy dictates how contracts are awarded and managed, including establishing departmental contracting authorities. The contracts in the sample exceeded the departmental authorities and therefore requisition forms had to be submitted to PWGSC in order to contract on Infrastructure Canada's behalf. Thus, Infrastructure Canada must submit a signed Form 9200, Requisition for Good and Services and Construction to PWGSC. In addition to requesting a contracting action, a signed form also indicates that funds have been committed to in the departmental financial system to meet contractual obligations (Federal Administration Act, Section 32 approval).

Infrastructure Canada's established business process is to have the dollar value indicated on a requisition form match the value of the signed contracts. This is also the value that is entered into the financial system as a commitment. Each amendment is processed with a new requisition. However, this was not the process used by the project team prior to May 2014. Up until this time, the project team was subject to the processes and procedures in place at Transport Canada.

In at least three out of the eight contracts examined, the contract requisition forms that were sent to PWGSC indicated a dollar value that was greater than the awarded contract value. This meant that PWGSC was authorized to contract with the supplier up to a dollar value that was greater than the dollar value of the contract. As such, the project team was able to amend contracts directly with the supplier and PWGSC without issuing new requisition forms or involving Infrastructure Canada's contracting group. This is important because the dollar value committed in the departmental financial system was only equal to the current value of the contracts and not the dollar value that PWGSC was authorized to contract up to. There is a risk that work could be performed for which there is no commitment in the departmental financial system to meet contractual obligations.

This highlights the risks and complications that may arise when a standard approach to contract management is not consistently applied. Given that the Finance and Contracting Directorate is responsible for managing contractual commitments in the financial system, officials from this Directorate need to be involved in the processing of all contract amendments developed by the project team. This would ensure a consistent approach and that funds will be available to pay suppliers for work performed.

5.2 Contract Payment Processes

Audit criteria for 5.2 Contract Payment Processes

It was expected that:

- Processes are in place to ensure payment for goods and services complied with Government of Canada legislation, as well as Treasury Board and Infrastructure Canada policies and directives.

Contract Payments

Conclusion:

Overall, the implementation of the controls established to pay for goods and services received as part of the project were not fully compliant with legislative and policy requirements. Immediate measures should be put in place to ensure that departmental financial delegations are working as intended. This includes strengthening controls related to section 33 and 34 of the Financial Administration Act.

The payment process for 5.2 Contract Payment Processes

The Financial Administration Act establishes the rules to oversee contract payment processes. Section 34 of the Act refers to the acceptance of work performed, goods supplied or services rendered. Section 33 indicates that prior to issuing payments, sections 32 (availability of funds) and 34 should be verified to ensure the relevant documentation to support the payment is complete and accurate, and that the payment is legal and in accordance with related appropriations. In addition, there are other policies and directives such as the Treasury Board Directive on Delegation of Financial Authorities for Disbursements and Directive on Account Verification that must be adhered to.

Documentation to support payment Framework for 5.2 Contract Payment Processes

There were generally two types of invoices:

- Those related to progress payments, hours worked, or reimbursement of costs (submitted with a progress statement, time sheet, or receipts); and

- Those related to payments for the delivery of a product such as equipment or a report.

We examined 15 progress payment invoices, 6 product payment invoices and the 2 invoices that were included on the confirming order, for a total of 23.

For all cases there was adequate supporting documentation on file to recommend payment. Specifically for product payment invoices, there was evidence of a project team member's receipt and acceptance of the deliverable. Finally, for the two entries related to the confirming order, there was adequate documentation to support payment.

Recommendation to Pay (Financial Administration Act - Section 34) for 5.2 Contract Payment Processes

While there was evidence that due diligence was performed on each invoice, the recommendation to pay was incomplete in four (4) of 23 instances. These issues related to a project manager indicating an incorrect fund centre on one section 34 approval and not dating section 34 signatures. The lack of a date on Section 34 could have an impact on determining when Canada accepted the deliverable, which may impact interest charges, among other things. Moreover, without a date, the ability to reconstruct the sequence of events and how the transactions were processed is compromised.

Payment Requisition (Financial Administration Act Section 33) for 5.2 Contract Payment Processes

Once fund centre managers review and approve invoices, they are sent to Accounting Operations for processing and payment. The departmental Delegation of Financial Signing Authorities delegates specific authorities outlined in the Financial Administration Act to specific positions. Prior to authorizing the release of payment (Section 33) certain conditions must be met – verifying financial commitments (section 32) and accepting receipt of goods or services (section 34).

Section 33 authorities are limited in certain circumstances. One such limitation includes the payment of invoices related to operating transactions in excess of $100,000. The Chief, Accounting Operations and Financial Systems (or higher) must authorize and sign section 33 for these types of payments. In five of the sampled items, the officer that signed Section 33 did not have authority to do so.

The same issue was previously reported in the Internal Audit of Information Technology Contracts in November 2011. Since that audit, measures had been implemented to correct these situations and strengthen account verification oversight by requiring formal quarterly reporting by the Head of Accounting Operations for payments over $100,000. However, this has not been conducted on a continuous basis.

6 CONCLUSION AND RECOMMENDATIONS

Overall, contract management and monitoring practices were generally compliant with relevant authorities and policies. However, the implementation of the controls established to pay for goods and services received were not fully compliant with legislative and policy requirements. Immediate measures should be put in place to ensure that departmental financial delegations are working as intended. This includes strengthening controls related to section 33 and 34 of the Financial Administration Act.

There are two recommendations:

- The Assistant Deputy Minister, Corporate Services Branch should ensure that Federal Montreal Bridges Branch officials responsible for contracts are trained on appropriate standard contract management practices and processes, including Financial Administration Act signatory requirements and the management of contract amendments.

- The Assistant Deputy Minister, Corporate Services Branch should establish controls to strengthen the section 33 approval process and to ensure that payments are authorized by an official with the appropriate delegated authority as per the departmental delegation of financial signing authorities.

Management response: Management accepts the recommendations and action plans have been put in place to address the two areas for improvement identified.

The audit findings, conclusions and recommendations relate only to Infrastructure Canada and do not reflect the management practices employed by any other department.

7 STATEMENT OF CONFORMANCE

The audit conforms to the International Standards for the Professional Practice of Internal Auditing and the Internal Auditing Standards for the Government of Canada as supported by the results of the quality assurance and improvement program.

8 MANAGEMENT RESPONSE AND ACTION PLAN

| # | Recommendation | Management Response and Action Plan | OPI and Due Date |

|---|---|---|---|

| 1 | The Assistant Deputy Minister, Corporate Services Branch should ensure that Federal Montreal Bridges Branch officials responsible for contracts are trained on appropriate standard contract management practices and processes, including Financial Administration Act signatory requirements and the management of contract amendments. | Accepted. Contracting and Procurement invited Federal Montreal Bridges officials and employees to an information session in June 2014 to discuss contract management practices and processes including Financial Administration Act signatory requirements and the management of contracts and amendments. This was in the early stages of their contract/file transfers from Transport Canada to Infrastructure Canada. It was well attended and successful in establishing Infrastructure Canada practices and processes. A mandatory follow up session to re-enforce internal procedures and practices will be provided to Federal Montreal Bridges staff with contract management responsibilities. | OPI:

ADM, Corporate Services and CFO

DATE: July 31, 2015 |

| 2 | The Assistant Deputy Minister, Corporate Services Branch should establish controls to strengthen the section 33 approval process and to ensure that payments are authorized by an official with the appropriate delegated authority as per the departmental delegation of financial signing authorities. | Accepted. The procedures put in place related to section 33 approvals and payment verification have been reinforced with financial officers and payments will be reviewed by the appropriate level of management. The Chief, Accounting Operations and Financial Systems met with all financial officers delegated with section 33 authority to reinforce their accountabilities and authority levels. Additionally, the Manager of Accounting Operations and Financial Systems will review the payment verification process and will make the necessary adjustments to strengthen the section 33 approval process. This will be done by the end of June 2015. | OPI: ADM, Corporate Services and CFO DATE: June 30, 2015 |

- Date modified: